The Rental Real Estate Tax “Trap”

Many people have the idea that rental real estate properties are a great way to financial freedom. In particular, the idea is build a portfolio of rental properties to generate ongoing income in retirement. While it is true that owning real estate and renting it out can be a great investment, there are many things a potential investor needs to consider. Today, the discussion is how rental real estate’s tax advantages eventually turn into a tax “trap.”

The Tax Benefit of Rental Real Estate Investing

The IRS treats rental real estate investing similar to owning a small business, because in reality it is a business. Just like a business, the rental investor can deduct from his rental income all expenses related to owning the property. Expenses include everything from property insurance and real estate taxes to minor repairs. If there is a mortgage on the property, the interest on the mortgage is also a deductible expense, but this isn’t any different than taking a loan for any other investment. Interest on loans used to purchasing investments of all sorts, including stocks and bonds, is tax deductible.

The real tax benefit of owning rental real estate is called depreciation. Depreciation is a tax term for allocating the cost of a capital asset (rental real estate) over a period of “expected use.” For Rental property, the cost is allocated over 29.5 years. An example may be helpful in clarifying what depreciation is meant to do.

Let’s assume you own a landscaping business. In order to operate your business, you have to purchase a few items, such as lawnmowers and trailers to pull around the equipment. Since these are expenses of the business, you want to write them off against the income of your business. This is reasonable, but the IRS doesn’t think you should write them off entirely in the year you purchase them. When you purchase a lawn mower, you expect it to last several years, so the tax code requires you to write it off over a predetermined time period (depreciated). In this case, the lawn mower and trailer are required to be written off over seven years. If you purchased these items for $7,000 you would write off, or depreciate, $1,000 per year for seven years (ignoring mid-year conventions and Section 179, more technical tax stuff).

The scenario is the same for rental property. If you purchase a rental property, then you get to depreciate the house (not the land) over 29.5 years. A house that has a cost basis of $150,000 would reduce the rental income you pay taxes on by $5,084 per year. That is over $1,250 in annual tax savings if the property owner is in the 25% bracket.

Why Depreciating Rental Real Estate is Different

Allocating the cost of business assets over their “expected life” makes sense from a certain perspective, but there is a significant difference between rental properties and most other business assets – capital gains. It is typical, though not guaranteed, for real estate to go up in value; the tax term for the increase in value is capital gains. If you own a lawn mower for seven years, the likelihood of it increasing in value is very close to zero, but the likelihood of a home going up in value over seven years (or 29.5 years) is very high. This is what leads to the tax trap – a combination of capital gains and depreciation recapture.

What is Depreciation Recapture?

Going back to the rental property with a cost basis of $150,000 in the house. Each year you, as the owner, write off (depreciate) $5,084 against the rental income. Assume after 10 years, you decide you want to sell the property and put the cash in your mattress; during that time, you will have depreciated $50,840 of the rental property’s value. If you sell the house for $150,000, or more, you will have to pay taxes on the amount depreciated – this is depreciation recapture.

The Entire Tax Trap – Bringing it Together

For simplicity, assume the value of the land didn’t increase or decrease in value. We will ignore the land completely and focus solely on the tax situation of the house (the actual building). Let’s also assume you are in the 25% tax bracket.

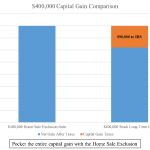

The $150,000 rental property generated $50,840 in depreciation over the 10 years, reducing the cost basis to $99,160. Assuming the house also increased in value by 3% per year, it is now worth $201,587. You can see this in the graph below.

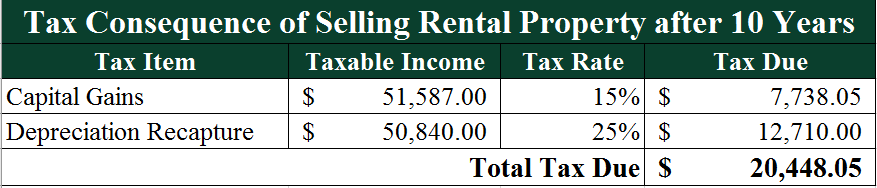

So what makes this a tax trap? The taxes! Your capital gains will be taxed at 15% and your depreciation recapture will be taxed at 25%. As you can see in the table below, selling the house will cause you to pay $20,448 in taxes! And that’s assuming the $102,427 in income you show on your tax return doesn’t push you into a higher tax bracket, which is very likely to happen.

Conclusion

The tax trap forces you to answer this important question – do I want to pay a large tax bill to sell my investment real estate or just keep the property indefinitely to put off the taxes? It is a decision each person has to make based on their own situation, but many people prefer not to pay taxes unless they have to. There are some strategies, such as attempting to qualify for the home sale exclusion or completing a 1031 exchange, that may help with the tax situation, but it depends on a number of different factors.

A taxpayer who is doing in depth tax planning may simply hold on to the property until there is a year where their income is very low or they have a large amount of capital losses to offset the capital gains. By planning the sale of the tax trap property to coincide with a lower income year, they will likely save thousands of dollars in taxes

If you enjoy learning how you could save thousands of dollars one day, don’t forget to sign up to receive every new blog update right to your email box.